Positioning for sterling volatility

Sterling has had a turbulent time since the Brexit referendum vote in June 2016. Should investors position themselves for sterling volatility to persist?

24 May 2019

A batch of data from different geographies is due next week as markets head towards the second half of the year.

In the US, investors await the second estimate on first-quarter gross domestic product and preliminary data on core personal consumption expenditure prices. Expectations are for a slowdown in personal consumption and weak inflation despite strong quarterly economic growth. Consumer confidence readings for May could start to show the impact on confidence of renewed trade tensions and softer data from the manufacturing sector.

On the other side of the Atlantic, markets brace themselves for a series of readings on economic sentiment in the eurozone and the UK. Data on money growth and private-sector lending, which are also out next week, are likely to continue showing signs of recovery.

In Asia, China will release the National Bureau of Statistics non-manufacturing and manufacturing purchasing managers’ index data for May. They are likely to show increased pressure after industrial production and fixed-asset investment slowed more than economists predicted last month.

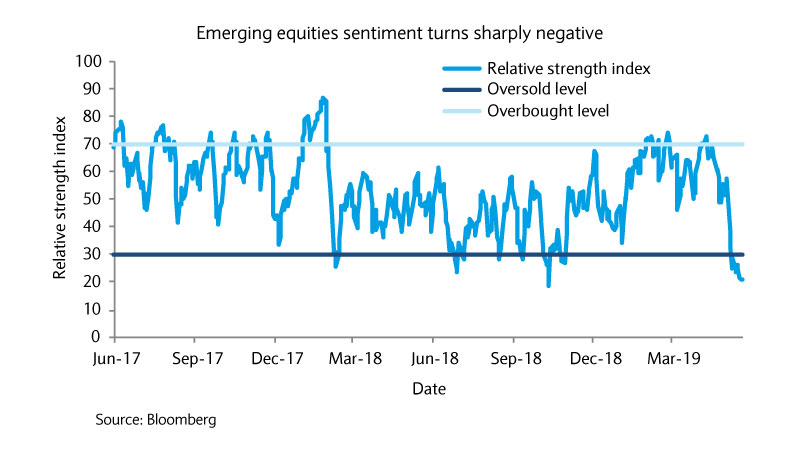

Asian stocks, as represented by the MSCI Asia Ex Japan Index, have been at the epicentre of investors’ concerns in May. Indeed, renewed trade tensions have caused Asian equities to lose more than half of their year-to-date gains in just three weeks. As a result of this significant pullback, the index now looks technically oversold, offering what could be an attractive entry point.

Although a further escalation in the US-China trade war could push Asian equities lower still, based on the current backdrop, we believe that the market may have overreacted in the short term. For instance, the relative strength index (or RSI) — which measures the magnitude of recent price changes to evaluate overbought or oversold conditions of a particular asset — has dipped below 30 for the first time this year in a sign that the recent downward move may have been too pronounced.

First, long-term fundamentals in the region remain supportive and Chinese authorities may provide further stimulus to the economy after a soft set of data in April. Second, with the market starting to question the likelihood of an economic rebound in China in the second part of the year, sentiment appears much more balanced, leaving room for positive surprises. Third, first-quarter earnings season offered reassurance that Chinese companies (around 40% of the index) will continue to grow steadily (+11% earnings growth).

In conclusion, in spite of all the geopolitical noise, we see no reason to deviate from our positive stance on emerging market equities in general and the Chinese market in particular.

Sterling has had a turbulent time since the Brexit referendum vote in June 2016. Should investors position themselves for sterling volatility to persist?

What do rising longevity trends globally mean for the healthcare sector?

This document has been issued by the Investments division at Barclays Private Banking and Overseas Services (“PBOS”) division and is not a product of the Barclays Research department. Any views expressed may differ from those of Barclays Research. All opinions and estimates included in this document constitute our judgment as of the date of the document and may be subject to change without notice. No representation is made as to the accuracy of the assumptions made within, or completeness of, any modeling, scenario analysis or back-testing.

Barclays is not responsible for information stated to be obtained or derived from third party sources or statistical services, and we do not guarantee the information’s accuracy which may be incomplete or condensed.

This document has been prepared for information purposes only and does not constitute a prospectus, an offer, invitation or solicitation to buy or sell securities and is not intended to provide the sole basis for any evaluation of the securities or any other instrument, which may be discussed in it.

Any offer or entry into any transaction requires Barclays’ subsequent formal agreement which will be subject to internal approvals and execution of binding transaction documents. Any past or simulated past performance including back-testing, modeling or scenario analysis contained herein does not predict and is no indication as to future performance. The value of any investment may also fluctuate as a result of market changes.

Neither Barclays, its affiliates nor any of its directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses (in contract, tort or otherwise) arising from the use of this communication or its contents or reliance on the information contained herein, except to the extent this would be prohibited by law or regulation..

This document and the information contained herein may only be distributed and published in jurisdictions in which such distribution and publication is permitted. You may not distribute this document, in whole or part, without our prior, express written permission. Law or regulation in certain countries may restrict the manner of distribution of this document and persons who come into possession of this document are required to inform themselves of and observe such restrictions.

The contents herein do not constitute investment, legal, tax, accounting or other advice. You should consider your own financial situation, objectives and needs, and conduct your own independent investigation and assessment of the contents of this document, including obtaining investment, legal, tax, accounting and such other advice as you consider necessary or appropriate, before making any investment or other decision.

THIS COMMUNICATION IS PROVIDED FOR INFORMATION PURPOSES ONLY AND IS SUBJECT TO CHANGE. IT IS INDICATIVE ONLY AND IS NOT BINDING.