Markets weekly

12 April 2019

Week ahead

April is going to give investors a lot to think about. We believe that depressed Manufacturing PMI, relative to still resilient Services PMI, might have overstated the actual slowdown happening in the manufacturing sector.

In that regard, February’s industrial production numbers in France and in the UK released last week were significantly better than expected. This would suggest that trade tensions have weighed on sentiment but not necessarily had the same impact on business so far.

Global economic health

The industrial production data for March in the US will be released on Tuesday. Expectations are for an increase of 0.3% month-on-month -an improvement from February’s flat number.

On Wednesday, it will be China’s turn to release its latest hard data. Industrial production, retail sales and fixed assets investment is likely to reflect the stimulus that was implemented at the beginning of the year.

It will also be interesting to see if the soft data starts to improve. Regional industrial surveys in the US are usually a good proxy for the ISM index coming out the following week. For this reason, the Empire Manufacturing survey on Monday and the Philadelphia Fed business survey on Thursday should not be overlooked.

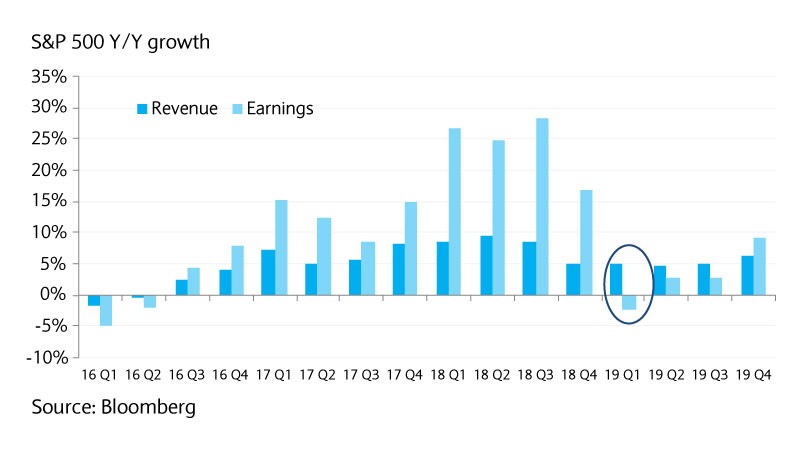

Chart of the week

This week marks the start of the earnings season for the first quarter of 2019 in the U.S. This period is usually a time for investors to disconnect from the political and macroeconomic noise and focus on what matters most over the long term: companies’ fundamentals.

In the context of an equity market that has rallied +15% this year and a yield curve that has inverted, there is a clear need for some good news. Unfortunately, this appears to be a big ask as, for the first time in three years, analysts expect companies in the S&P 500 index to experience a contraction in earnings. Yet, we believe that reality may be less dramatic than our chart of the week implies.

View the latest edition of Markets Weekly

Investments can fall as well as rise in value. Your capital or the income generated from your investment may be at risk.

This document has been issued by the Investments division at Barclays Private Banking and Overseas Services (“PBOS”) division and is not a product of the Barclays Research department. Any views expressed may differ from those of Barclays Research. All opinions and estimates included in this document constitute our judgment as of the date of the document and may be subject to change without notice. No representation is made as to the accuracy of the assumptions made within, or completeness of, any modeling, scenario analysis or back-testing.

Barclays is not responsible for information stated to be obtained or derived from third party sources or statistical services, and we do not guarantee the information’s accuracy which may be incomplete or condensed.

This document has been prepared for information purposes only and does not constitute a prospectus, an offer, invitation or solicitation to buy or sell securities and is not intended to provide the sole basis for any evaluation of the securities or any other instrument, which may be discussed in it.

Any offer or entry into any transaction requires Barclays’ subsequent formal agreement which will be subject to internal approvals and execution of binding transaction documents. Any past or simulated past performance including back-testing, modeling or scenario analysis contained herein does not predict and is no indication as to future performance. The value of any investment may also fluctuate as a result of market changes.

The value of any investment may also fluctuate as a result of market changes.

Neither Barclays, its affiliates nor any of its directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses (in contract, tort or otherwise) arising from the use of this communication or its contents or reliance on the information contained herein, except to the extent this would be prohibited by law or regulation..

This document and the information contained herein may only be distributed and published in jurisdictions in which such distribution and publication is permitted. You may not distribute this document, in whole or part, without our prior, express written permission. Law or regulation in certain countries may restrict the manner of distribution of this document and persons who come into possession of this document are required to inform themselves of and observe such restrictions.

The contents herein do not constitute investment, legal, tax, accounting or other advice. You should consider your own financial situation, objectives and needs, and conduct your own independent investigation and assessment of the contents of this document, including obtaining investment, legal, tax, accounting and such other advice as you consider necessary or appropriate, before making any investment or other decision.

THIS COMMUNICATION IS PROVIDED FOR INFORMATION PURPOSES ONLY AND IS SUBJECT TO CHANGE. IT IS INDICATIVE ONLY AND IS NOT BINDING.