Inflation prospects are a hot topic for investors. To prepare for different inflation scenarios over the next twelve months, we investigate which asset classes might best shield portfolios against inflation surprises. A diversified, multi-asset class portfolio including commodities, inflation- linked bonds, selected equity styles and shorter duration bonds may be one potential solution.

Diversification is the bedrock of a long-term investment process. Crafting a portfolio that will be resilient and robust in different macroeconomic environments, requires careful consideration of key systematic risks. Currently, one of the main questions facing investors is whether the recent spikes in inflation are merely transitory or might become permanent.

Inflation risk in the spotlight

Inflation erodes wealth over time. Historically, sustained inflation has been a headwind for both equities and bonds. Interest rates typically rise with inflation, which, in turn, hurts bond prices. Equity valuations can be hit at higher inflation levels as well. Consequently, the correlation between the two asset classes can move to positive territory when inflation is rising persistently.

Given the elevated levels of inflation and inflation uncertainty, over the short and medium term, it is important to consider which investment strategies might shield portfolios from inflation.

Our analysis is based on asset return sensitivities (or betas) to unexpected inflation over a one-year horizon. Arguably, at any point in time, expected inflation is already “priced in” by financial markets. Therefore, we investigate how to position portfolios optimally ahead of potential significant inflation surprises.

Lulled by the 2010s

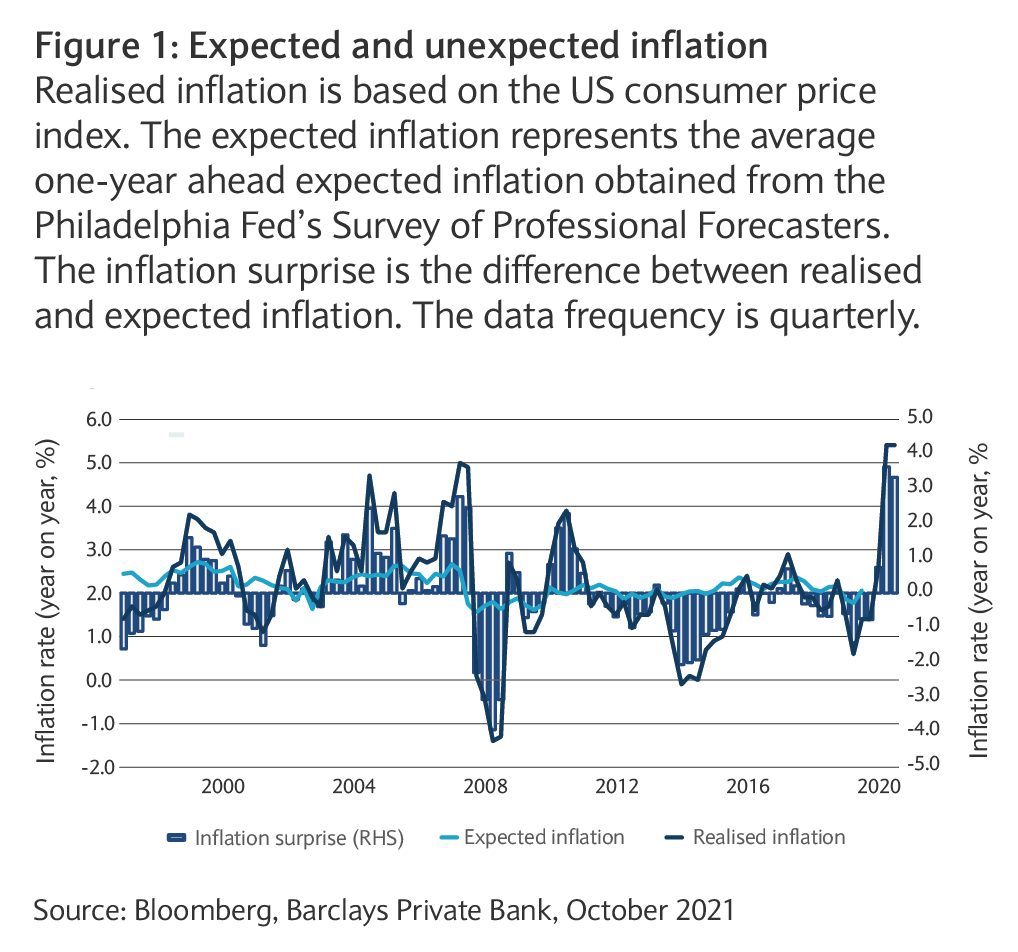

Following the global financial crisis of 2008-09, investors witnessed a decade that was characterised by secular stagnation (see figure 1). Weak growth, meagre inflation, low interest rates and quantitative easing left a strong footprint on financial markets.

Ageing populations, suppressed commodity prices, technological changes and reduced production costs due to globalisation, have been the main disinflationary drivers in the last decade. Many investors wondered if inflation would again reach worrying levels in major developed economies crawling back above the central bank target levels.

But the genie is out of the bottle

Initially, the pandemic-induced lockdowns and a strong shift in consumer sentiment unlocked additional disinflationary factors. Governments and monetary authorities acted swiftly, with a battery of monetary and fiscal policies.

Following the reopening of economies around the globe, inflation started to pick up in 2021. This was driven by several factors.

One upward pressure on prices comes from strong pent-up demand, high household savings and a massive increase in the money supply. Supply-chain disruptions, including soaring shipping costs and container shortages, only amplified the demand-side effect. Finally, the base effect should not be neglected – low prices twelve months ago boost the year-on-year inflation rate during the re-opening and recovery.

Inflation prospects

In our view, it is unlikely that powerful forces which kept inflation in check during the 2010s will easily wane.

Therefore, our baseline scenario is that the inflation rise is only transitory and it is expected to fade away in the short- to-medium term. However, there are several risks that may materialise, and keep inflation elevated for some time.

Geopolitical tensions and trade wars might resurface and offset some of the benefits of globalisation. Consequently, potential “reshoring” and “nearshoring” of companies to, or close to, home markets may increase production costs.

Government debt is at historically high levels, and it is possible that central banks will take a more flexible view of inflation targeting (note that the US Federal Reserve now uses long-term average inflation when targeting) and allow short and medium-term overshooting of the past reference levels.

The greening effect

The transition to green economies may also create inflationary pressures. So-called “greenflation” might emerge from different sources. Fighting the climate risk and reducing the environmental footprint will probably incur higher costs for companies through substantial capital expenditure, and research and development investments.

Higher labour costs associated with wage increases, and costs associated with investments in equality and diversity could be the second factor. Last, but not least, regulatory requirements regarding sustainable development need certain organisational changes, and may incur productivity costs.

Taming inflation surprises with diversification

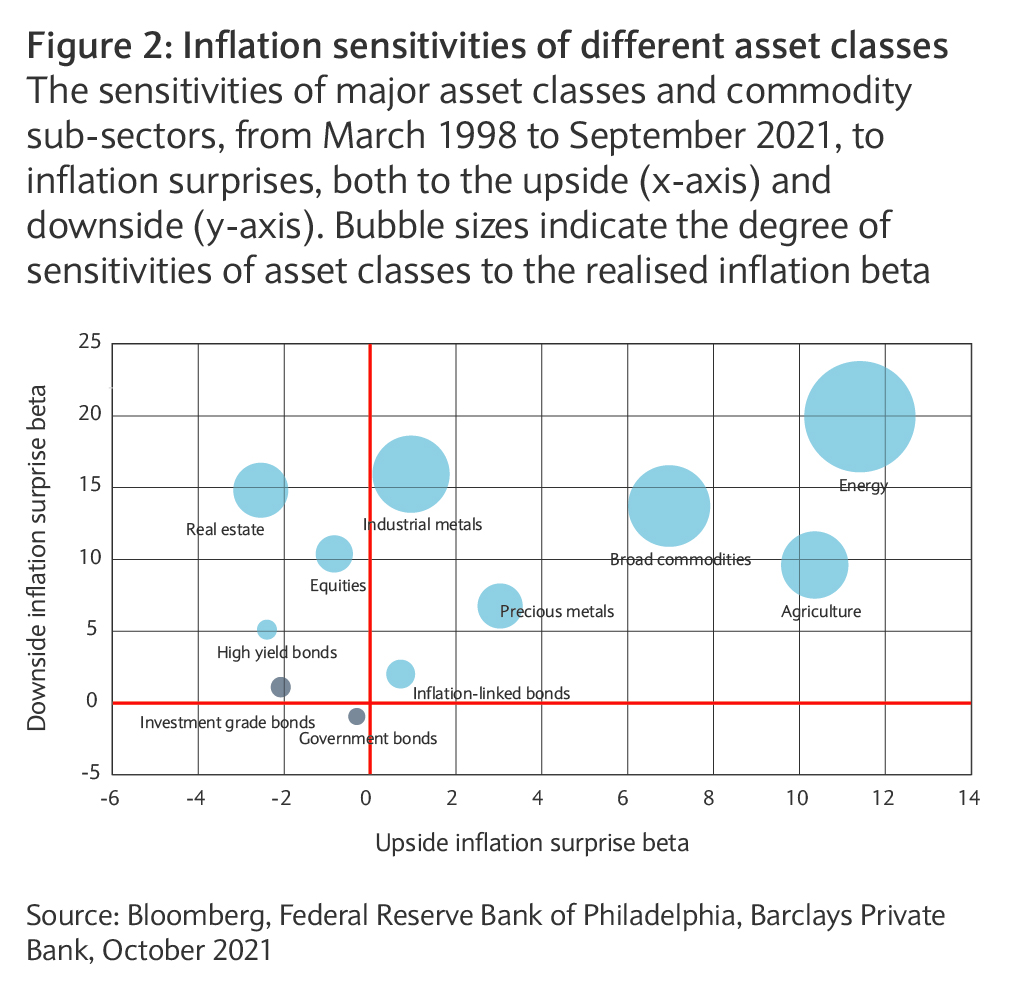

Measuring inflation beta, or the sensitivity of an asset class to realised inflation, can help us understand which assets might be used as an inflation hedge. However, to build an effective hedge against unexpected inflation, an understanding of how different asset classes react to, upside and downside, inflation surprises is needed.

In our analysis (see figure 2), we consider only significant deviations from expected inflation (more than 0.5% in either direction). This is because it is difficult to disentangle small inflation surprises from other factors that can influence asset performance, such as economic growth.

Classy commodities

Commodities are the best hedges against upside inflation surprises in our review period. In particular, energy and industrial metals outperform when there is an unexpected spike in inflation. This is expected, as these commodity sub-sectors are the key inputs in the industrial production process.

Precious metals can also be used as an upside inflation hedge. Although they do not perform as strongly as energy when inflation spikes, they are one of the best choices among commodities as a downside-inflation hedge. This is a reason why gold is considered as one of the best portfolio diversifiers.

The convenience of inflation-linked bonds

On an asset classes level, inflation-linked bonds (ILBs) represent the second-best inflation hedge (see Solving the puzzle of a post-pandemic bond world). This is expected as ILBs – by design – automatically adjust in a rising inflation environment.

However, it is important to consider also the breakeven inflation as well, which represents the market-implied future inflation rate.

Short duration might help nominal bonds

On average, nominal bonds are under pressure when inflation spikes because interest rates tend to rise in parallel.

However, the losses can be controlled to a certain extent by overweighting shorter duration bonds in a portfolio, irrespectively of their credit risk exposure. However, we note that nominal government bonds provide protection if inflation surprised on the downside.

Hidden equity gems

Investing in stocks provides a direct growth exposure. In the case of rising inflation, companies should be able to pass on higher costs to consumers (see The post-COVID investor outlook as we shift from pandemic to endemic). In practice, this process changes at a different pace for each industry. To gain further insights into how equities react to bouts of unexpected inflation, we extend our analysis to styles.

Our results are intuitive – growth and momentum provide the best protection against upside inflation surprises.

Quality is neutral to inflation spikes, whereas value, high dividend and low volatility do not provide protection in strong inflationary scenarios.

In a strong deflationary scenario, none of the equity sectors provides protection. This is because such events typically coincide with an economic recession when equities sell off.

Thinking beyond – thinking crypto

Recently, cryptocurrencies have been flagged by some investors as a potential inflation hedge. We do acknowledge some similarities between cryptocurrencies and gold, such as uniqueness, scarcity, and transactability. However, it is unclear if a parallel can be drawn between the two assets.

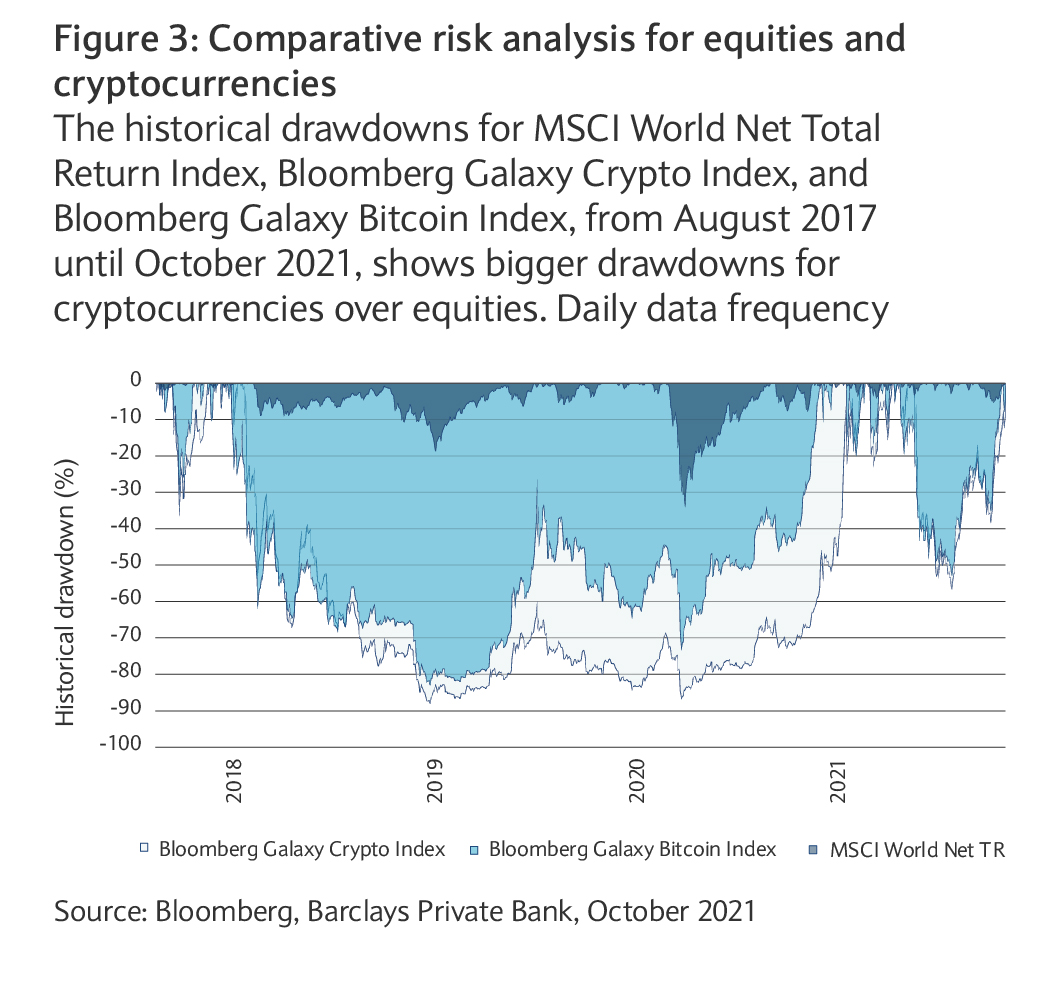

Cryptocurrencies are a recent invention and represent highly speculative digital assets. There are many opportunities, but for most investors the risks are prohibitively high. We estimated the historical drawdowns for bitcoin and a basket of cryptocurrencies over the past four years (see figure 3).

These drawdowns illustrate past losses from investing at highs, and the time it would have taken to recover those losses. The maximum historical drawdown is 80-90% and the recovery time is close to three years. Over the same period, global equities experienced drawdowns of up to 35% and much shorter recovery times.

Additionally, we think that the investment landscape is largely under construction and can dramatically change over just a couple of months. It remains to be seen how the crypto universe will consolidate and address potential regulatory challenges in the future.