Market Perspectives March 2021

Encouraging hopes of a vaccine-driven recovery are keeping investors in good spirits.

05 March 2021

8 minute read

By Julien Lafargue, CFA, London UK, Head of Equity Strategy

High hopes of a vaccine-driven recovery and encouraging reported earnings have powered many equity markets to record levels. Given potential vaccine problems, timing of fiscal and monetary policy retreats and threats of inflation, are valuations overstretched?

We started the year with a constructive but somewhat cautious outlook, expecting more muted returns. Two months in and global equities have already jumped as much as 6%, pushing towards our bull case scenario. Given possible surprises lying ahead, the risk-reward remains balanced but the road is likely to be bumpy.

While we expected companies to post better-than-expected results in the final three months of 2020 (Q4), we have been positively surprised by the magnitude of the beats. In the US, with more than 80% of companies surpassing the consensus’ forecast, fourth-quarter earnings growth is on track to reach 3.5% versus an 8% decline expected initially. This is an amazing outcome given that COVID-19 did not exist a year ago. Indeed, expected earnings for the following twelve months are picking up (see chart).

In Europe, the picture is more mixed as, despite an 18% positive average surprise, Q4 earnings have contracted by at least 15%. Most of this difference can be explained by the significant divergence in index composition, Europe being much more exposed to the energy and financial sectors and less to technology.

Back in November, we highlighted a fair value for the S&P 500 at around 3,700. At the time, much better fundamentals seemed required to justify upside from that level. With much stronger-than-expected Q4 earnings, this year’s numbers have a more solid base on which to grow.

As a result, our estimate of equity markets’ fair value has moved a few percentage points higher, closer to the initial bull case (in the 3,900-4,000 range on the S&P 500). This point estimate assumes recovery throughout the year, supported by accommodative monetary and fiscal policies and a successful COVID-19 vaccination campaign in the most of the developed world.

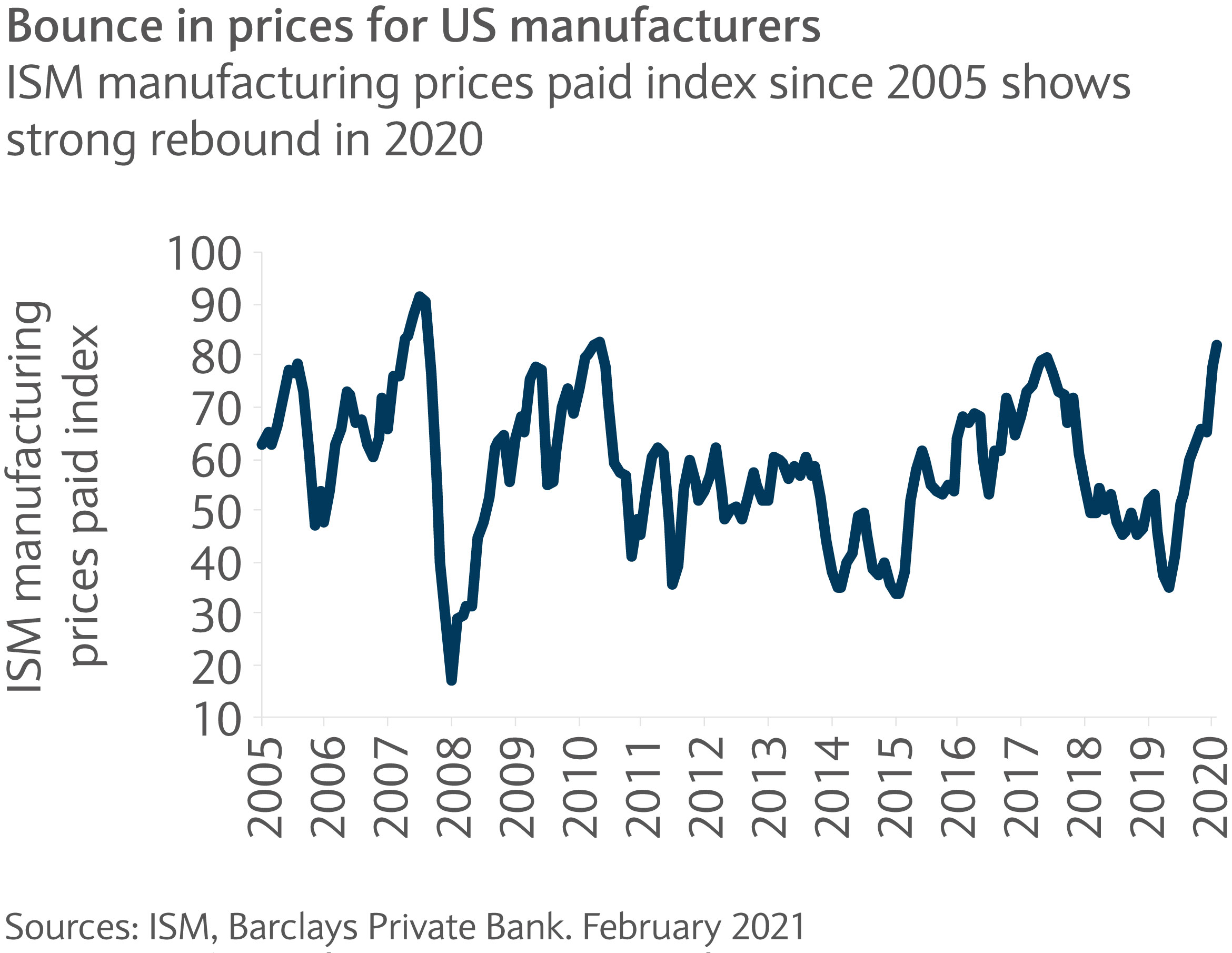

The above assumptions are optimistic and leave the door open to disappointment should any of them fail to deliver. At the top of the “wall of worry” is inflation. Indeed, the topic has attracted much attention in the last few months. The combination of base effects, recovery, higher commodity prices and stress in some value chains (semiconductors in particular) point to a potentially sharp increase in prices ahead. The prices paid by US manufacturers already seem to be climbing (see chart).

While a temporary surge in inflation could be managed, the real risk lies with a sustained rise in prices. Though moderate inflation (as opposed to deflation risk) may be welcome, persisting negative interest rates in Europe and very low ones in the US are not appropriate for a world where the Phillips curve, or inverse relationship between inflation and unemployment, re-establishes itself.

Recalibrating monetary policy to prevent the economy from overheating would require central banks to adopt a much tighter stance, possibly putting pressure on equity valuations as finally there would be an alternative to stocks.

Outside of the obvious risk of seeing the pandemic becoming a feature of the world we live in for years, preventing a full recovery, the other possible issue worth highlighting is linked to fiscal stimulus.

The key reason why economies and markets have been able to recover so quickly from the pandemic shock is the unparalleled government bail outs offered during the crisis. For now, the taps remain open and the commitment to do “whatever it takes” is intact. However, as the debt burden and budget deficits balloon, at some point governments may have to pull the plug.

It may seem premature to think about fiscal retrenchment. But if and when stimulus is reversed, whether due to political or market (perhaps rising bond yields) pressures, the real impact of the pandemic could be felt.

The result would be a surge in bankruptcies, a spike in unemployment rates and a much bleaker outlook for companies. This would compromise current expectations for a strong earnings recovery and force asset prices to drop. Such a miscalculation might be met with additional monetary support eventually but it would certainly leave a mark.

Much positive news already seems to be discounted by the market and in our fair value estimate. We see two main upside risks though.

The first one relies on even stronger-than-anticipated earnings growth. As January’s US retail sales figures suggested (up 5.3% month on month versus 1.0% expected), pent-up demand might be significantly higher than initially thought.

The second upside risk could be a faster-than-expected return to normal as COVID-19 becomes nothing more than a regular flu. That said, this appears an unlikely scenario in the short term. However, science has shown it can deliver results at an unprecedented pace. The combination of vaccines capable of fighting variants of the virus and better treatments for infected people could allow some of the most affected areas of the economy (travel and leisure in particular) to recover ahead of plan.

The above-mentioned possible catalysts are known unknowns and can be more easily factored in by market participants. The real risk lies in events that few, if any, see coming. The COVID-19 pandemic was an extreme example of this, but such curveballs are frequent.

Earlier this year, the Reddit-based retail investors frenzy caused some short-lived volatility as hedge funds were forced to reduce their gross exposure. Thankfully, this phenomenon did not last for long but it shows that surprises can result in significant volatility.

Because “black swan” events are unpredictable, risks are largely impossible to discount and can only be mitigated via proper diversification. This is why we encourage investors to adopt a balanced approach when building portfolios.

Although the upside at the index level may be limited, investment opportunities can be found. Indeed, with elevated expectations and limited visibility, significant dispersion at both the sector and the stock level seems likely.

Wider dispersion in returns calls for a more active approach to investing, using stock picking to unearth alpha in a world were beta might be less relevant. Our focus remains on “quality” investing, favouring resilient free cash flow generation and attractive medium-term growth prospects.

Encouraging hopes of a vaccine-driven recovery are keeping investors in good spirits.

This communication:

Any past or simulated past performance including back-testing, modelling or scenario analysis, or future projections contained in this communication is no indication as to future performance. No representation is made as to the accuracy of the assumptions made in this communication, or completeness of, any modelling, scenario analysis or back-testing. The value of any investment may also fluctuate as a result of market changes.

Barclays is a full service bank. In the normal course of offering products and services, Barclays may act in several capacities and simultaneously, giving rise to potential conflicts of interest which may impact the performance of the products.

Where information in this communication has been obtained from third party sources, we believe those sources to be reliable but we do not guarantee the information’s accuracy and you should note that it may be incomplete or condensed.

Neither Barclays nor any of its directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses (in contract, tort or otherwise) arising from the use of this communication or its contents or reliance on the information contained herein, except to the extent this would be prohibited by law or regulation. Law or regulation in certain countries may restrict the manner of distribution of this communication and the availability of the products and services, and persons who come into possession of this publication are required to inform themselves of and observe such restrictions.

You have sole responsibility for the management of your tax and legal affairs including making any applicable filings and payments and complying with any applicable laws and regulations. We have not and will not provide you with tax or legal advice and recommend that you obtain independent tax and legal advice tailored to your individual circumstances.

THIS COMMUNICATION IS PROVIDED FOR INFORMATION PURPOSES ONLY AND IS SUBJECT TO CHANGE. IT IS INDICATIVE ONLY AND IS NOT BINDING.