Can equities weather a hike in inflation?

01 April 2021

By Julien Lafargue, CFA, London UK, Head of Equity Strategy

You’ll find a short briefing below. To read an in-depth analysis of this article, please select the ‘full article’ tab.

-

Summary

Key takeaways

- Vaccine-fuelled recovery to drive strong earnings comparisons with last year

- US inflation likely to rise, though global inflation may well be lower

- Equity risk premiums are looking healthier

- ”Quality” stocks still appeal as a long-term investment.

A year ago, much of the world was in lockdown. Today, vaccines are being quickly administered in many developed economies and several are planning their grand reopening. This stark difference in the macroeconomic backdrop means that earnings comparisons with last year should be strong. One variable in particular has grabbed the headline, causing some concern for investors: inflation.

Powerful base effects, higher oil prices and supply chain disruptions have pushed inflation expectations higher. In the US, economists polled by Bloomberg anticipate that the consumer price index (CPI) will reach 3% in the second quarter and average 2.4% in 2021.

Meanwhile, in the eurozone, the consensus expects CPI of 1.5% this year. While this is much higher than the 0.3% recorded in 2020, it is still well below the European Central Bank’s target of 2%. Globally, inflation looks like being around 2.8% this year, below last year’s 3.2%.

Inflation can influence equities in two ways:

Firstly, while companies’ revenues should increase following higher selling prices, the result on profits could be negative if input costs rise further.

Secondly, if inflation is accompanied by higher real bond yields, the discount rate applied to future cash flows will increase, compressing valuations, all else being equal.

In February’s Market Perspectives we argued that, all else equal, a yield of 1.6% on US 10-year government bonds could push up the equity risk premium (ERP) to levels consistent with negative equity returns over the next five years.

Since then, the strong fourth-quarter earnings season helped to support the earnings yield. At current valuations, the ERP would fall below its 40th percentile (250 basis points) when 10-year bond yields approach 2%, leaving some room for manoeuvre.

S&P 500 equity risk premium in 2021 31 January 26 March S&P 500 level 3,850 3,974 S&P 500 earnings per share ($) 169 180 SPX price-to-earnings ratio 22.7 22.1 Earnings yield 4.4% 4.5% 10-year government bond yield 1.10% 1.67% Equity risk premium 331 285 This year’s sharp rise in bond yields has triggered significant sector moves. As an investment style, “value” has finally started to outperform (the MSCI World Value is outperforming its growth counterpart by 10% this year, as at 26 March 2021). However, this is negligible in light of the divergence that has occurred at the industry and stock level.

Fundamentally, we continue to think that owning “quality” companies makes sense over the long term. While they may initially struggle against their value peers in a strong recovery scenario, over time, they are likely to deliver better risk-adjusted returns.

With the prospect of higher inflation seemingly looming, investors might focus on companies, industries and sectors offering pricing power.

-

Full article

Fears of a sustained rise in inflation has hit sentiment for equities, despite a vaccine-driven recovery moving closer. But the impact of inflation on earnings expectations affects sectors, and companies, differently. We look at the potential winners and losers. That said, investing in “quality” companies over the long term can help to ride out any inflation-induced turbulence.

A year ago, much of the world was in lockdown. Today, vaccines are being quickly administrated in many developed economies and several are planning their grand reopening. This stark difference in the macroeconomic backdrop means that earnings comparisons with last year will be undoubtedly strong. One variable in particular has grabbed the headline, causing some concern for investors: inflation.

Moderately higher prices ahead

Powerful base effects, higher oil prices, supply chain disruptions (for items like semiconductors and freight) and a strong recovery have pushed inflation expectations higher. In the US, economists polled by Bloomberg anticipates that the consumer price index (CPI) will reach 3% in the second quarter and average 2.4% in 2021.

While this marks a sharp acceleration from recent trends, it is far from hyperinflation. In fact, in 2018, US inflation was 2.5%. In addition, the personal consumption expenditures (PCE) indicator, the US Federal Reserve’s preferred measure of inflation, shows more muted price pressures.

The central bank expects the PCE to reach 2.2% this year and 2.0% next year. So while we are likely to see higher US prices in coming months, there seems little to worry about, in our opinion.

Mainly a US issue

Interestingly, inflation dynamics appear more muted outside America. In the eurozone, the consensus expects CPI of 1.5% this year. While this is much higher than the 0.3% recorded in 2020, it is still well below the European Central Bank’s target of 2%. Globally, inflation looks like being around 2.8% this year, below last year’s 3.2%.

A healthy development

Although it might sit at the top of several investors’ concerns, moderate and controlled inflation may not be much of an issue. In fact, from both a macroeconomic and financial markets’ perspective, higher prices can be much healthier than much lower ones: deflation. As such, slightly higher CPI should be welcomed as the reflection of a strong recovery.

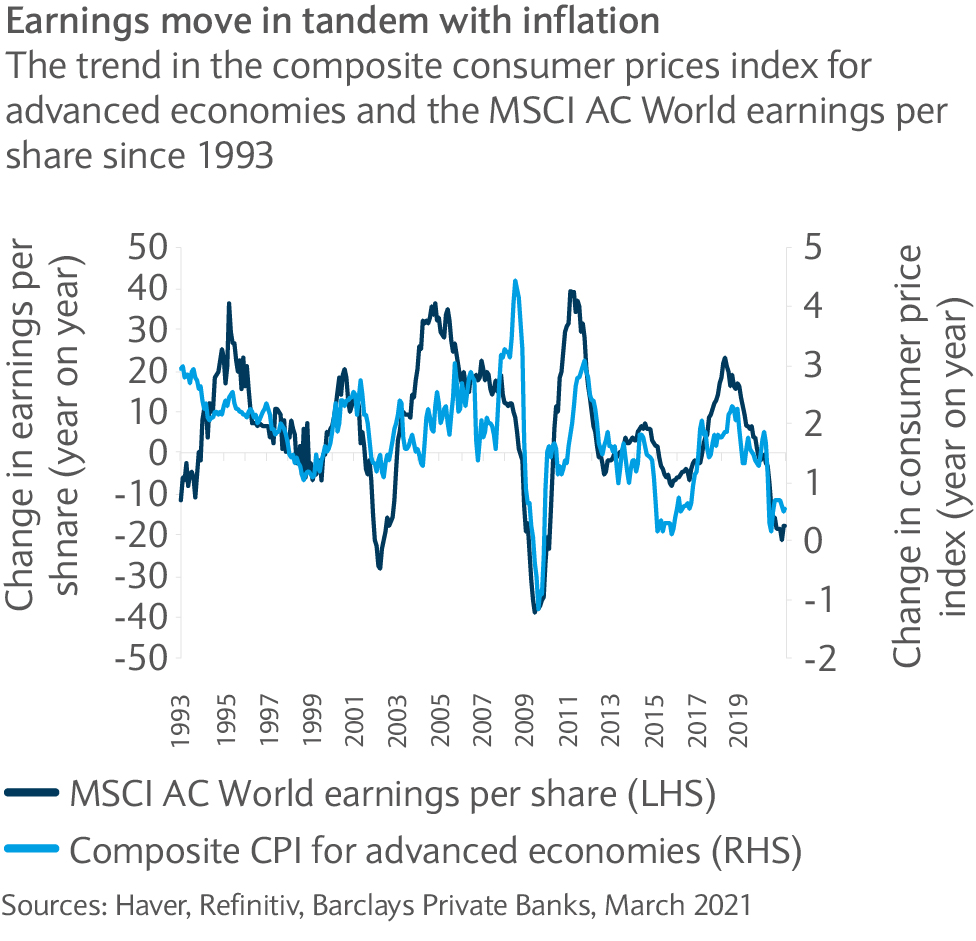

Historically, equities have performed well when inflation was in the 2-3% range (see chart). This is because higher prices typically mean more sales as these are recorded in nominal terms. Unfortunately, in the current context of extremely low interest rates and extended equity valuations, a sudden rise in inflation could cause short-term volatility.

How higher prices can affect equities

Inflation can influence equities in two ways. First, while companies’ revenues should increase following higher selling prices, the result on profits could be negative if input costs rise faster. In this context, pricing power is essential to counteract the risk of margin compression.

The second risk equities face is related to interest rates. If inflation is accompanied by higher real bond yields, the discount rate applied to future cash flows will increase, compressing valuations, all else being equal. With companies offering strong and steady growth being most at risk of a change in the discount rate, this phenomenon could fuel the sector rotation we’ve seen this year.

Keeping an eye on the equity risk premium

We highlighted the relationship between interest rates and equity valuations in February’s Market Perspectives. At that time, we argued that, all else equal, a yield of 1.6% on US 10-year government bonds could push the equity risk premium (ERP), to levels consistent with negative equity returns over the next five years.

Since then, the strong fourth-quarter earnings season helped to support the earnings yield. At current valuations, the ERP would fall below its 40th percentile (250 basis points) when 10-year bond yields approach 2%, leaving some room for manoeuvre (see table).

S&P 500 equity risk premium in 2021 31 January 26 March S&P 500 level 3,850 3,974 S&P 500 earnings per share ($) 169 180 SPX price-to-earnings ratio 22.7 22.1 Earnings yield 4.4% 4.5% 10-year government bond yield 1.10% 1.67% Equity risk premium 331 285 Looking beneath the surface

While interest rates may not pose an immediate risk to equities, this year’s sharp rise in bond yields has triggered significant sector moves. As an investment style, “value” has finally started to outperform (the MSCI World Value is outperforming its growth counterpart by 10% this year, as at 26 March 2021). However, this is negligible in light of the divergence that has occurred at the industry and stock level.

While the 25% gain in energy shares this year, as of 26 March, is more a function of the stronger oil price, financials (+14% in the same period) and banks in particular (+20%) have been key beneficiaries of higher interest rates. By comparison, defensive, bond-proxy, sectors such as utilities and consumer staples have lagged (flat over the same period). While we would expect this rotation to fade, it reinforces our conviction that investors should ensure appropriate diversification.

Quality and pricing power

Fundamentally, we continue to think that owning “quality” companies makes sense over the long term. While they may initially struggle against their value peers in a strong recovery scenario, over time, they are likely to deliver better risk-adjusted returns. Remember that quality is not synonymous with “defensive” or technology assets and maintaining some exposure to cyclicality in portfolios seems preferable, in our view.

With the prospect of higher inflation seemingly looming, investors might also focus on companies, industries and sectors offering pricing power. Below, we list the most likely impact of higher prices at the sector and industry level, helping to find potential winners and losers should inflation climb. However, the outcome could vary for each company within each sector. This makes active management even more relevant.

Sector Expected impact of higher inflation and interest Consumer discretionary Luxury is probably one of the sectors with the highest pricing power.

Car manufacturers, unlike part suppliers, tend to have little ability to increase prices and material expenses can account for almost two-thirds of revenues for some companies. In addition, they can be victims of both temporary (say freight costs and semiconductor shortages) and secular (say electrification and digitalisation) factors pushing up costs.

Leisure tends to have limited exposure to inflation. In travel, airlines can often pass on higher oil prices to consumers but this takes time. On the other hand, asset-light hotel management companies appear better positioned than travel companies given their lack of exposure to labour and property price inflation.

Consumer staples Food/household good producers tend to have some pricing power. However, because of heightened competition, their ability to pass on costs has weaken recently. To be sustainable and rewarded, price increases should happen with added value (such as a health-focused product or having a sustainability angle). So if pricing power returns, it is likely to be a function of this innovation rather than simple pass- through effects.

For distributers (such as supermarkets) inflation is usually positive. Again, though, their ability to pass on cost increases through higher prices may be limited, especially when unemployment levels are elevated.

Tobacco companies (and to some extent producers of alcoholic drinks) typically have strong pricing power given the inelasticity of demand for their products.

Energy and materials As commodity producers, these sectors can profit from higher raw materials prices. However, they have no pricing power. In fact, they are price takers and can only realise the market price of the underlying commodity they produce. Pricing power appears further down the value chain. Chemicals companies, in particular, have frequently been able to increase prices over time as they add value to – and represent a key link in – the manufacturing process. Financials There isn’t much pricing power in this sector (with the exception of some insurance companies). Yet, the sector remains an “inflation play” because higher inflation typically brings higher interest rates and a steeper yield curve. However, this environment could be negative for non-life insurers as it could boost costs of general insurance claims and challenge their bond-proxy status. Healthcare Healthcare isn’t really exposed to “macroeconomic” inflation. There is certainly some pricing power driven by innovation but, ultimately, the regulatory framework is key in allowing healthcare companies to increase prices. From a valuation perspective, more than interest rates, investor sentiment is a risk as healthcare could lag in a recovery scenario. Industrials Because of the value added they provide, most specialised industrial companies should be able to hike prices. However, this may take a couple of quarters to materialise. Infrastructure plays could benefit from higher inflation as their revenue is often indexed to economic growth and inflation trends. However, higher interest rates would likely challenge their valuations. Technology Inflation, as it is generally driven by input costs, should have limited impact on companies producing software. Hardware producers are likely to be more impacted, especially in light of the shortage of semiconductors being experienced of late. Semiconductor manufacturers have already started to boost prices but they also are ramping up capital expenditure to meet increased demand. While the manufacturers have strong pricing power, with most share prices having doubled in the last two years, it may be too late to play the “inflation” theme through this industry. Telecoms In Europe in particular, the high degree of competition among operators makes telecommunications a highly deflationary business with very limited ability to raise prices. Mobile tower companies tend to be better positioned as they usually have more protection from inflationary pressures but valuations may suffer from higher interest rates. Utilities The impact will probably be mixed at best as even companies with indexation built into their revenue allowances may see their share prices struggle due to their negative correlation to bond yields.

Related articles

Investments can fall as well as rise in value. Your capital or the income generated from your investment may be at risk.

This communication:

- Has been prepared by Barclays Private Bank and is provided for information purposes only

- Is not research nor a product of the Barclays Research department. Any views expressed in this communication may differ from those of the Barclays Research department

- All opinions and estimates are given as of the date of this communication and are subject to change. Barclays Private Bank is not obliged to inform recipients of this communication of any change to such opinions or estimates

- Is general in nature and does not take into account any specific investment objectives, financial situation or particular needs of any particular person

- Does not constitute an offer, an invitation or a recommendation to enter into any product or service and does not constitute investment advice, solicitation to buy or sell securities and/or a personal recommendation. Any entry into any product or service requires Barclays’ subsequent formal agreement which will be subject to internal approvals and execution of binding documents

- Is confidential and is for the benefit of the recipient. No part of it may be reproduced, distributed or transmitted without the prior written permission of Barclays Private Bank

- Has not been reviewed or approved by any regulatory authority.

Any past or simulated past performance including back-testing, modelling or scenario analysis, or future projections contained in this communication is no indication as to future performance. No representation is made as to the accuracy of the assumptions made in this communication, or completeness of, any modelling, scenario analysis or back-testing. The value of any investment may also fluctuate as a result of market changes.

Barclays is a full service bank. In the normal course of offering products and services, Barclays may act in several capacities and simultaneously, giving rise to potential conflicts of interest which may impact the performance of the products.

Where information in this communication has been obtained from third party sources, we believe those sources to be reliable but we do not guarantee the information’s accuracy and you should note that it may be incomplete or condensed.

Neither Barclays nor any of its directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses (in contract, tort or otherwise) arising from the use of this communication or its contents or reliance on the information contained herein, except to the extent this would be prohibited by law or regulation. Law or regulation in certain countries may restrict the manner of distribution of this communication and the availability of the products and services, and persons who come into possession of this publication are required to inform themselves of and observe such restrictions.

You have sole responsibility for the management of your tax and legal affairs including making any applicable filings and payments and complying with any applicable laws and regulations. We have not and will not provide you with tax or legal advice and recommend that you obtain independent tax and legal advice tailored to your individual circumstances.

THIS COMMUNICATION IS PROVIDED FOR INFORMATION PURPOSES ONLY AND IS SUBJECT TO CHANGE. IT IS INDICATIVE ONLY AND IS NOT BINDING.