Market Perspectives May 2020

Financial markets have rebounded strongly from a vicious sell-off, following an exceptional policy response to the COVID-19 outbreak. But volatility is likely to be high for some time.

01 May 2020

7 minute read

By Michel Vernier, CFA, London UK, Head of Fixed Income Strategy

Emerging market bond yields seem attractive on paper, but risk remains high, given the COVID-19 crisis, and is unevenly spread among countries. While there are opportunities available in the region, selection will be key.

The poor economic prospects and ultra-loose monetary policy in the wake of the COVID-19 pandemic has depressed global rates. In the US, yields on bonds with short maturities are anchored close to the US Federal Reserve’s (Fed) target rate while the 10-year yield is poised to trend even lower again. Fears of a significant rate sell off, perhaps caused by a ballooning fiscal balance and a resulting oversupply of bonds, seem premature at this stage.

The Fed will likely absorb a large part of the debt supply for some time. After the credit crisis in 2008, for example, the Fed only began communicating its intention to scale back bond purchases in 2013, sparking the “taper tantrum” rates sell-off. The overall trend in rates in the medium term will likely be dominated by large disinflationary pressures caused by very high unemployment rates, a lack of pricing power and lower energy prices. Only in the longer run longer dated bonds could potentially be exposed to inflationary pressures.

In our April Market Perspectives, we focused on developed market corporate bonds, risks in various sectors and the BBB segment in particular, in light of the COVID-19 pandemic. We also discussed the effect of the recent Fed bond facilities. In this edition we take a closer look at emerging market bonds.

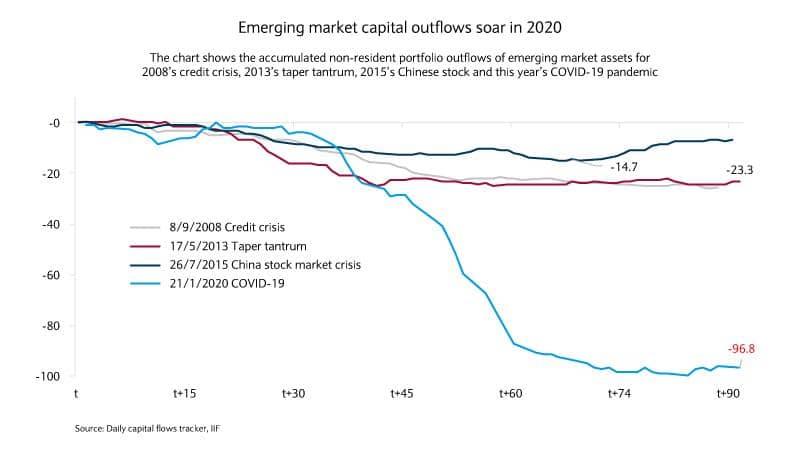

The asset class witnessed $31bn of outflows in March, the second largest monthly outflow since October 2008, as investors exited risk assets. That said, outflows from emerging market (EM) equities have topped those from EM debt each month this year and are substantially higher than those out of EM debt. A whopping $96.8bn has been withdrawn from EM equity and fixed income assets combined by non-emerging market residents, exceeding those seen in previous crises (see chart) by some margin.

In April the level of capital flows out of emerging market assets declined, somewhat, while the average difference (or spread) between US dollar-denominated EM bonds compared to US treasuries fell to 620 basis points, with the average yield of the former being 6.7%. Still, both the spread and average bond yield are at the highest levels since 2008. The difference in yields on offer from bonds in different regions or countries (or spread dispersion) is also very high, being a reminder that risk within the EM segment varies substantially

Despite relatively appealing yield levels, the risk of further substantial spread widening looks as high as ever, in part due to potential refinancing challenges and unsustainable deficits in some EM countries. The proportion of bonds trading at distressed prices among EM high yield-rated issuers is 36% and half of Asian high yield bonds are trading with a spread wider than 1,000 bp.

While the level of distressed bonds can be a good indicator for future default rates, historically speaking the spread compensation was sufficient to compensate for the losses seen from realised defaults thereafter. The implied compensation is now as high as it was in 2008’s credit crisis and is suggestive of a default rate of 9-10% compared to the current rate of 1.5%.

Many weaker countries are being uncomfortably exposed by the COVID-19 crisis. EM central banks have cut interest by almost 3,000 bp in aggregate and most countries have announced fiscal support packages.

However, many countries seem to lack urgency in their policy response or simply don’t have the financial resources to withstand a larger period of containment.

Many countries seem to lack urgency in their policy response or simply don’t have the financial resources to withstand a larger period of containment

The most prominent examples are Argentina and Lebanon which already announced a restructuring of their foreign bonds resulting in substantial "haircuts" for investors. Those sovereigns where large current account deficits and large debt service payments meet low direct investments and low foreign exchange reserves will be most vulnerable.

While defaults or imminent debt restructuring do not seem that likely, we believe that countries like Sri Lanka, Honduras, Angola or Turkey are particularly exposed which makes respective bonds vulnerable for further volatility. Upcoming bond redemptions in these countries are material in the context of the respective available foreign exchange reserves.

While International Monetary Fund (IMF) support facilities are in place, the fund will focus on the weakest countries, mainly in Africa. The majority of the IMF facilities come with prohibitive conditions and countries like Turkey or South Africa are trying to avoid seeking them.

Emerging market governments, like those in the developed world, are tackling the pandemic in different ways. While Brazil’s president is playing down the severity, India (with a population of 1.3bn) is pursuing a full containment strategy without having sufficient testing kits in place. The inconsistency and limited fiscal resources is a concerning combination.

For many EM countries, the COVID-19 crisis means a decline in the crucial revenue contribution made by commodities, especially oil. In judging the impact this is having on economies, it is important to consider factors like the price at which the external balance between imports and exports is at zero (known as the external breakeven price).

An oil price below a country’s breakeven price may require a country to take on more debt to fund the deficit. The breakeven level is high for Bahrain, Oman and Qatar and comparatively low in Russia or the United Arab Emirates for example. Substantial sovereign wealth assets for the latter two countries, for example, should help support them through this period.

While spreads are elevated and potentially cover future default losses, we think EM bonds are likely to face more volatility. Although appealing investment opportunities may arise, selection and active management will be key in order to weather the challenging times ahead.

Financial markets have rebounded strongly from a vicious sell-off, following an exceptional policy response to the COVID-19 outbreak. But volatility is likely to be high for some time.

Barclays Private Bank provides discretionary and advisory investment services, investments to help plan your wealth and for professionals, access to market.

This document has been issued by the Investments division at Barclays Private Banking division and is not a product of the Barclays Research department. Any views expressed may differ from those of Barclays Research. All opinions and estimates included in this document constitute our judgment as of the date of the document and may be subject to change without notice. No representation is made as to the accuracy of the assumptions made within, or completeness of, any modeling, scenario analysis or back-testing.

Barclays is not responsible for information stated to be obtained or derived from third party sources or statistical services, and we do not guarantee the information’s accuracy which may be incomplete or condensed.

This document has been prepared for information purposes only and does not constitute a prospectus, an offer, invitation or solicitation to buy or sell securities and is not intended to provide the sole basis for any evaluation of the securities or any other instrument, which may be discussed in it.

Any offer or entry into any transaction requires Barclays’ subsequent formal agreement which will be subject to internal approvals and execution of binding transaction documents. Any past or simulated past performance including back-testing, modeling or scenario analysis contained herein does not predict and is no indication as to future performance. The value of any investment may also fluctuate as a result of market changes.

Neither Barclays, its affiliates nor any of its directors, officers, employees, representatives or agents, accepts any liability whatsoever for any direct, indirect or consequential losses (in contract, tort or otherwise) arising from the use of this communication or its contents or reliance on the information contained herein, except to the extent this would be prohibited by law or regulation..

This document and the information contained herein may only be distributed and published in jurisdictions in which such distribution and publication is permitted. You may not distribute this document, in whole or part, without our prior, express written permission. Law or regulation in certain countries may restrict the manner of distribution of this document and persons who come into possession of this document are required to inform themselves of and observe such restrictions.

The contents herein do not constitute investment, legal, tax, accounting or other advice. You should consider your own financial situation, objectives and needs, and conduct your own independent investigation and assessment of the contents of this document, including obtaining investment, legal, tax, accounting and such other advice as you consider necessary or appropriate, before making any investment or other decision.

THIS COMMUNICATION IS PROVIDED FOR INFORMATION PURPOSES ONLY AND IS SUBJECT TO CHANGE. IT IS INDICATIVE ONLY AND IS NOT BINDING.